In brief

- The insurance industry has access to vast amounts of data that can be leveraged to gain insights and create business value.

- However, many firms struggle to extract meaningful insights from it. Data needs to be integrated from disparate sources such as customer interactions and social media.

- Implementing advanced analytics techniques such as machine learning can help insurers unlock the business value from their data by enabling more accurate predictions and personalized services.

It will come as no surprise to hear that CEOs and CIOs receive masses of promotional material

covering the latest and greatest developments in technology.

Some items explore things like

how to use smartwatches to gain a competitive edge. Others are about building

car-tracking devices and using the data to better-price the risk, all the while championing

a safer driving style or using automation to simplify the offering —

removing the need to make a claim even.

It’s only a matter of time before these small-scale

experiments lead to a breakthrough in the relationship between customer and insurer, causing a

near-revolution that will mean the end of the road for companies unable to adapt.

Handling data at scale

We’re not trying to tell you how to run your business, but organizations are creating and storing

more data than ever. And significant modern terms such as automation, AI and customer 360, all

require an ability to handle data at scale that, previously, was never an issue.

This is

nothing new, though. Insurance has always been a data-handling business. But what is new, is the

scale of this phenomenon.

Exploiting industry trends

This is the first in a series of three blogs covering insurance industry trends, and what your

company needs to do to capitalize on them.

Most of the trend ideas have been with us for

years one way or another, but ease of use is the new black — a fresh slant makes all the difference.

Two decades ago, building a customer base or meeting regulatory requirements were tedious tasks and,

while competition was tough, the market was more or less closed to new players.

Generating added value

Today, the situation is much different. There are lots of global and local organizations generating

huge volumes of data and trying to figure out how to use it to deliver more value. Providing

insurance, explicitly or not, is one of the attractive directions for adding value to existing

products. So, insurance companies face some tough choices. Should they respond? If yes, then

how?

There are no easy answers, particularly with the enormous pressure to be more efficient

in a traditional way without actually changing the nature of the business done. It will work until

new market entrants disrupt the market, segment by segment.

Winning the broker game

Insurance price comparison sites are profitable as long as players have similar risk models and use

a common set of more-or-less standard questions. Change is unwelcome because it generates work — new

questions and workflows need to be implemented, and the comparison site operator might not be

willing to do that just for one provider. And even if the work is done, customers may not be willing

to answer a single question.

The overall situation stops insurance companies innovating and,

so far, the only way forward has been to establish a better brand-customer relationship. There is

another way forward — augmenting the data that the customer has typed in with the data acquired from

different sources in real time.

Making fact-based decisions

For instance, instead of asking where a car is usually parked, you could use data obtained from the

owner’s mobile phone provider to identify the driver. Then, assess how well he or she drives the

car, based on their Bluetooth black box. The availability of this kind of information would reduce

the administrative burden on customers in many situations and, even if it didn’t, it could help

insurers identify dishonest customers.

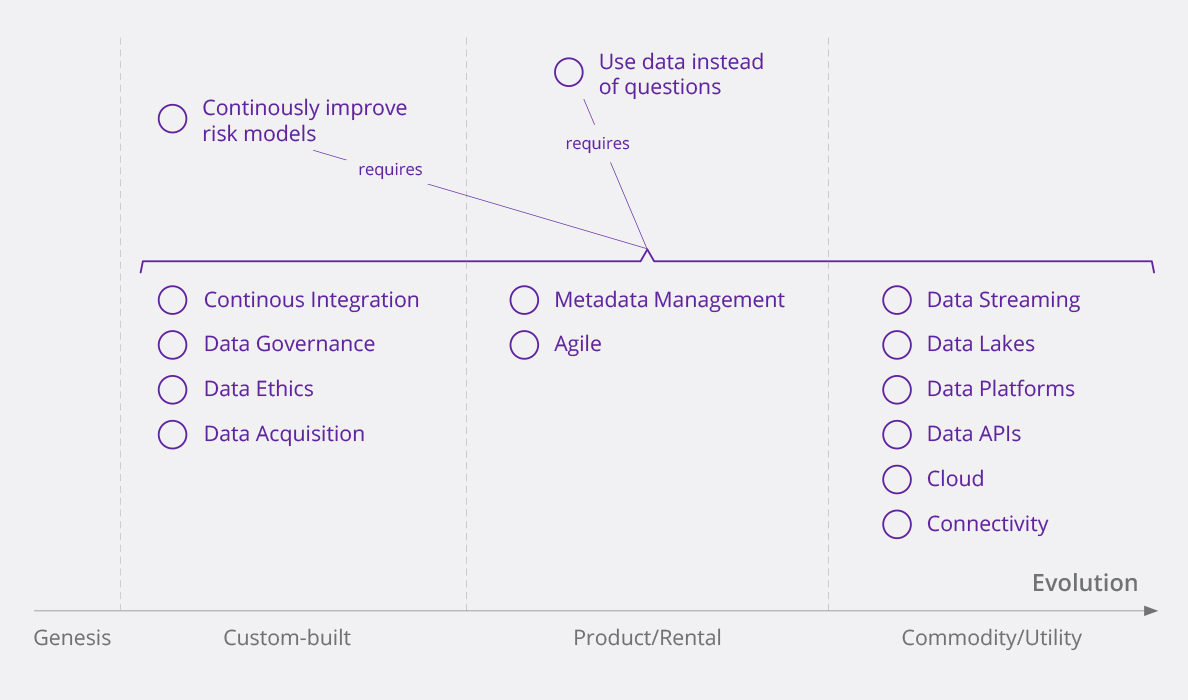

There are a few components that could be implemented

to enable this sort of operation.

Figure 1: Which components do you need?

Reviewing data ethics

Clearly, many of the necessary components are in place — data streaming, lakes,

platforms, APIs and so on. Cloud and connectivity are readily available too. However, you might need

help creating the mechanisms for collecting and integrating the data, and you’ll need to consider

the ethics of controlling and using the data.

This might mean building proof of concept (PoC)

models and minimum viable products (MVP), which could be accelerated by using an appropriate

InsurTech firm and working with modern Agile technology experts who have experience in the sector.

Applying the aggregator model

In future, the crossover into wider industry will become more apparent. It will be

possible to open the same APIs that aggregators use for other commodity-type providers (carmakers,

smartphone producers, airlines, etc.). Indeed, the rise of food distribution businesses like

Deliveroo is bringing the aggregator model to food shopping too.

The insurance sector has

ceded a lot of control to the aggregator, and is trying to regain that control just as the retail

sector is beginning a slow waltz with a new type of aggregator. The key question for a retailer

entering such an arrangement would be, “is my brand strong enough to retain market share, and does

quality become a lower driver than price?”.

Sharing expert opinion

Various industry experts contributed to this three-part series of blogs, drawing on market

experience, tech knowledge and current customer base to draw their conclusions. You can read the

next blog: Calculate insurance risk more precisely and turbocharge your digital customer

experience and the third blog: Monetize the

customer data you didn’t even know you had.

DXC is the leading provider

of core insurance technology globally, with over 1,900 insurance customers serviced by over 18,500

professionals.

Adaptix, DXC’s Analytics and Engineering business, is the preferred

partner for banks undertaking strategic transformation, and is providing fresh insight into

insurance sector analytics. To learn more, contact: financialservices@adaptix.com

Jeremy Owenson

![]()

During his 12 years with Zurich Insurance, Jeremy gained extensive market knowledge, from sales and the underwriting process to claims and even outsourcing (including offshore). Now, he’s concentrating on how technology can revolutionize the industry. Leveraging DXC Adaptix Solutions’s leading position in Banking and Capital Markets, Jeremy is determined to bring fresh ideas and ML-driven underwriting to the insurance sector.

Krzysztof (Chris) Daniel

![]()

Chris specializes in strategic planning and technology evolution. He is also a Wardley Mapping practitioner (a tool and technique for visual communications, risk reduction, situational awareness and change management, which helps us understand, influence and predict the future). Chris’ primary focus is on the identification, development and use of mapping in use cases like outsourcing, project management, restoring the balance of power and emerging financial frameworks.